Americans are carrying more than $1.3 trillion in credit card debt, a huge amount that continues to climb. The average U.S. household now owes more than $11,000 in credit card debt.

However, credit card debt isn’t impacting everyone equally.

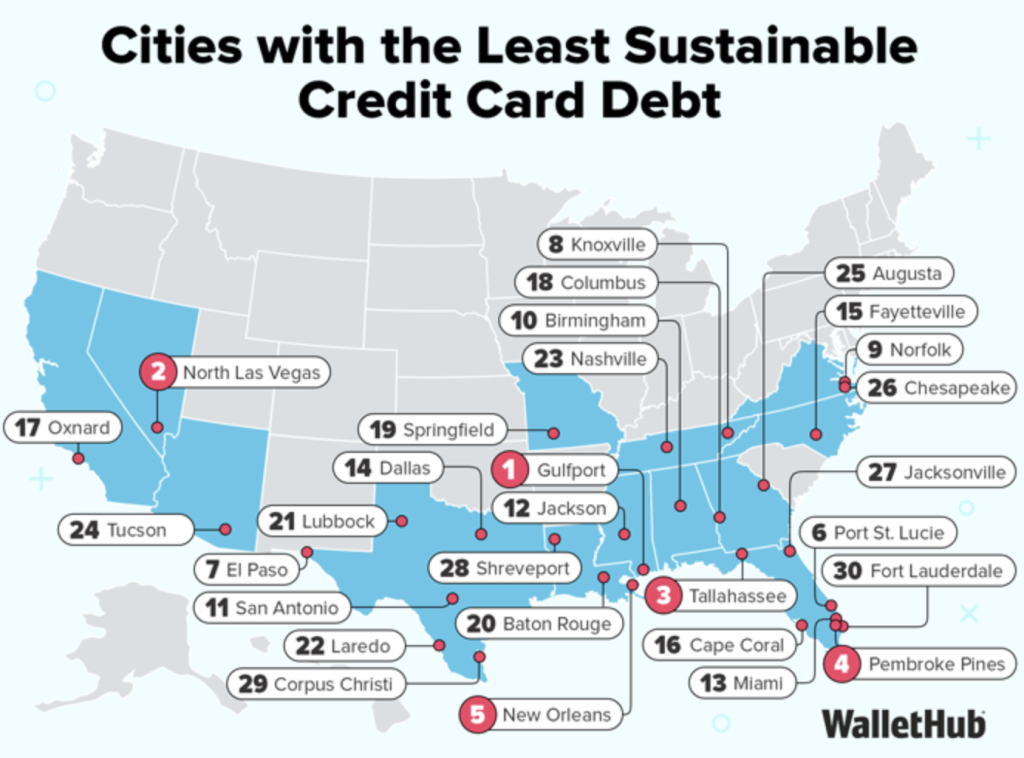

To find out where Americans are having the most problems managing their debt, WalletHub, a personal finance website, analyzed TransUnion credit data to estimate the cost and time needed to pay off median credit card balances in more than 180 U.S. cities.

In the cities where people are having the most problem with credit card debt, residents tend to have low median incomes, which contributes to larger than average credit card debts, Chip Lupo, WalletHub analyst, said in the report “Cities With the Most and Least-Sustainable Credit Card Debt.”

“As a result, people are only able to make small payments on their debts each month, stretching out the amount of time to get debt-free to as long as 9 years,” Lupo said. “This can lead to thousands of dollars in interest payments – in some cases, more interest than the amount of debt they currently owe.”

Cities where people are having the most problems with credit card debt:

1.Gulfport, Miss.

2. North Las Vegas, Nev.

3. Tallahassee, Fla.

4. Pembroke, Fla.

5. New Orleans, La.

6. Port St. Lucie, Fla.

7. El Paso, Texas

8. Knoxville, Tenn.

9. Norfolk, Va.

10. Birmingham, Ala.

Cities where people are having the least problems paying off credit card debt:

173.Worcester, Mass.

174. Washington, D.C.

175. Columbia, Md.

176. Madison, Wisc.

177. Seattle, Wash.

178. Irvine, Calif.

179. Jersey City, N.J.

180. San Jose, Calif.

181. San Francisco, Calif.

182. Fremont, Calif.

As the WalletHub map shows, people in the South are having the most problems with credit card debt:

Report highlights offer details on why people are struggling:

Gulfport, Miss., has the highest credit card debt problems, with a median balance of $2,997 and a payoff timeline more than 105 months, nearly nine years. Gulfport residents take a long time to pay off their credit card debts in part because their median earnings are very low, at $42,689 per year. That’s the sixth-lowest among the 182 cities in the study.

North Las Vegas, Nev., has the second highest credit card debt problems among 182 of the largest U.S. cities. It will take residents with debt an average of nearly 100 months, 8.3 years, to pay off what they owe. Some of the reasons behind North Las Vegas’ long credit card pay-off timeline includes the city’s high median credit card debt, $3,271, and relatively low median earnings for workers, $47,405. Residents will end up paying an average of $3,618 in interest by the time they get debt-free, according to WalletHub calculations.

Residents of Tallahassee, Fla., have the third highest credit card debt problems, because it would take an average of nearly 95 months, nearly eight years, to pay off the typical balance. The median credit card debt is $3,252, and the cost of the interest over eight years is more than the original balance – at $3,380.

What to do about high credit card debt:

Tahereh Alavi Hojjat, Ph.D., professor of economics at DeSales University, offers these tips for reducing credit card debt:

Create and stick to a budget: Develop a realistic budget that considers increased costs due to inflation. Prioritize essential expenses and allocate funds accordingly.

Put money in an emergency fund: Build a replenished emergency fund to cover unexpected expenses. This can prevent reliance on credit cards for unforeseen costs.

Limit non-essential spending: Evaluate and prioritize purchases based on necessity.

Prioritize high-interest debt: Focus on paying down high-interest debts first to minimize interest payments. Consider consolidation debts to lower interest rates.

Use credit wisely: Be cautious with credit card usage and avoid unnecessary debt. Pay off credit card balances in full each month.

Explore income boosting opportunities: Seek additional income sources – part-time work or freelancing.

Invest wisely: Evaluate investment strategies that provide returns exceeding inflation. Diversity investment can lower overall risks.

For credit counseling, watch out for debt relief companies that are ripoffs.

Contact the National Foundation for Credit Counseling to get advice on how to eliminate your credit card debt.